In today’s rapidly evolving business landscape, staying ahead of the curve is paramount. One technology that has emerged as a game-changer, revolutionizing industries and operations, is blockchain. This groundbreaking technology is not just a passing fad but a transformative force with the potential to reshape the way businesses operate, interact, and thrive.

From supply chain management to financial services, blockchain is making its mark across diverse sectors. Its decentralized, transparent, and secure nature offers unprecedented opportunities for businesses to streamline processes, enhance efficiency, and unlock new avenues for growth. This article delves into the exciting world of blockchain technology in business, exploring its applications, benefits, and the profound impact it is having on industries worldwide.

Demystifying Blockchain: Concepts and Applications

Blockchain technology has emerged as a transformative force, revolutionizing industries and redefining how businesses operate. At its core, blockchain is a decentralized, immutable, and transparent ledger that records and verifies transactions across a network of computers. This technology is gaining immense traction due to its ability to enhance security, efficiency, and trust in various business processes.

A blockchain is essentially a chain of blocks, each containing a record of transactions. These blocks are linked together cryptographically, ensuring the integrity and immutability of the data. Once a transaction is recorded on a blockchain, it cannot be altered or deleted, creating a permanent and verifiable record. This immutability makes blockchain ideal for applications requiring high levels of security and transparency.

The decentralized nature of blockchain means there is no single point of control or failure. Instead, the network is distributed across multiple computers, ensuring resilience and eliminating reliance on a central authority. This distributed architecture empowers participants to verify transactions independently, fostering trust and accountability.

Blockchain technology offers a wide range of applications across diverse industries. In finance, it enables faster, more secure, and cost-effective cross-border payments. Supply chain management benefits from increased transparency, traceability, and reduced fraud. Healthcare can leverage blockchain to securely store and share patient data, enhancing privacy and interoperability. Additionally, blockchain has applications in voting systems, digital identity verification, and intellectual property management.

How Blockchain Works: A Simple Explanation

Imagine a digital ledger that records transactions in a secure and transparent way. This ledger is distributed across a network of computers, making it extremely difficult to tamper with. That’s essentially what blockchain is. It’s a revolutionary technology that has the potential to transform various industries.

Here’s a simplified explanation of how it works:

1. Transactions: Each transaction is recorded as a block on the blockchain. A block contains information like who sent what to whom.

2. Verification: Before a block is added to the blockchain, it must be verified by multiple computers on the network. This process is known as mining.

3. Chain Formation: Once verified, the block is added to the blockchain, forming a chain of blocks. Each block is linked to the previous one, creating a permanent and tamper-proof record.

4. Decentralization: The blockchain is decentralized, meaning it doesn’t rely on a single authority. This makes it highly secure and resistant to manipulation.

In essence, blockchain offers a secure and transparent way to record and track information. It eliminates the need for a central authority, reducing the risk of fraud and manipulation.

Key Features of Blockchain: Transparency, Security, and Immutability

Blockchain technology is revolutionizing industries and operations, and at the heart of this revolution lie its key features: transparency, security, and immutability. These features, combined, create a robust and trustworthy system that fosters trust and efficiency across diverse applications.

Transparency refers to the open and auditable nature of blockchain. Every transaction is recorded on a public ledger, accessible to anyone. This transparency fosters trust and accountability, as all participants can see the history of transactions and verify their authenticity.

Security is another cornerstone of blockchain. Transactions are encrypted and protected by sophisticated cryptographic algorithms. This makes it extremely difficult for malicious actors to tamper with data or commit fraud. The decentralized nature of blockchain further strengthens its security, as there is no single point of failure.

Immutability means that once a transaction is recorded on the blockchain, it cannot be altered or deleted. This immutability creates a permanent and reliable record of transactions, ensuring data integrity and preventing fraud.

These three key features – transparency, security, and immutability – form the bedrock of blockchain technology. They empower businesses to build trust, streamline operations, and unlock new opportunities across various industries.

Blockchain Use Cases Across Industries

Blockchain technology is rapidly gaining traction across diverse industries, revolutionizing operations and transforming traditional business models. Its decentralized, transparent, and secure nature provides a robust foundation for innovative solutions, impacting sectors like finance, healthcare, supply chain, and more. Here are some of the key blockchain use cases across industries:

Finance: Blockchain is streamlining financial transactions, enabling faster and more secure cross-border payments, facilitating secure digital asset management, and enhancing transparency in financial markets.

Healthcare: Securely storing and sharing sensitive patient data, facilitating interoperability between healthcare systems, enabling efficient drug tracking and provenance, and accelerating medical research are key applications of blockchain in the healthcare industry.

Supply Chain: Blockchain is revolutionizing supply chains by providing real-time visibility into product movement, enhancing traceability and authenticity, combating counterfeit products, and improving inventory management.

Government: Blockchain can be leveraged to streamline government processes, ensuring secure voting systems, verifying identities and credentials, and improving transparency in public procurement.

Real Estate: Blockchain is simplifying and accelerating real estate transactions, facilitating secure property ownership, and enabling automated escrow services.

Energy: Blockchain technology is supporting the development of decentralized energy grids, facilitating peer-to-peer energy trading, and enabling efficient renewable energy credit management.

Gaming: Blockchain is enabling the creation of decentralized and transparent gaming platforms, fostering new forms of in-game assets and economies, and empowering players with greater control over their gaming experiences.

As blockchain technology matures and evolves, its applications across industries will continue to expand, driving further innovation and transforming the way businesses operate.

Supply Chain Management: Enhancing Transparency and Traceability

Blockchain technology is revolutionizing various industries, and supply chain management is no exception. Its inherent features of transparency and traceability are transforming how businesses operate, offering unparalleled visibility and trust throughout the supply chain.

Traditionally, supply chains have been complex and opaque, making it difficult to track goods and materials. This lack of transparency can lead to inefficiencies, fraud, and reputational damage. Blockchain addresses these challenges by providing a secure and immutable ledger of transactions, ensuring data integrity and authenticity.

By recording every transaction and movement of goods on the blockchain, businesses can track products from origin to end-user. This real-time visibility empowers them to monitor inventory levels, identify potential bottlenecks, and make informed decisions to optimize their supply chains.

Furthermore, blockchain enhances traceability, allowing consumers to gain insights into the origin and journey of their products. This increased transparency fosters trust and builds stronger relationships with customers who value ethical and sustainable practices.

The potential benefits of blockchain in supply chain management are vast. From reducing counterfeiting and fraud to improving efficiency and sustainability, this technology is poised to reshape the industry, making it more transparent, traceable, and resilient.

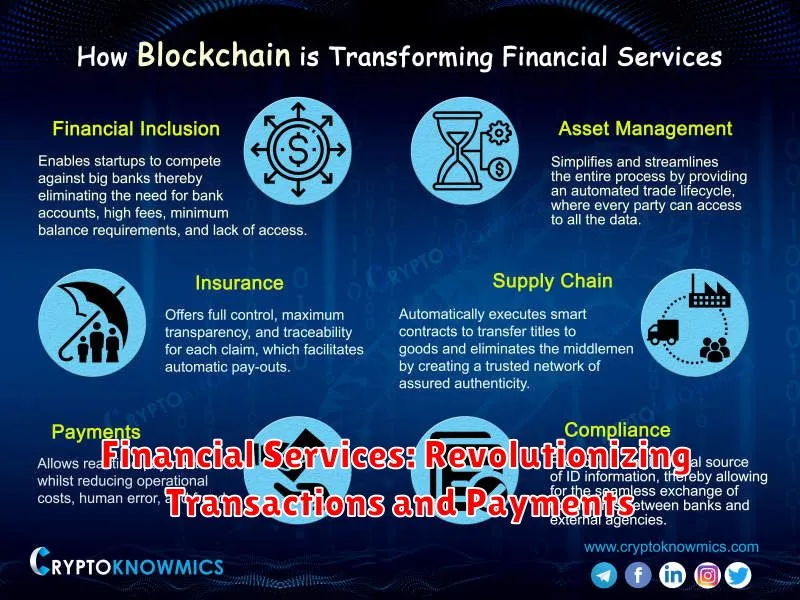

Financial Services: Revolutionizing Transactions and Payments

The financial services industry is experiencing a seismic shift driven by the emergence of blockchain technology. This revolutionary technology is transforming traditional financial processes, paving the way for faster, more secure, and more transparent transactions and payments.

Blockchain’s decentralized nature eliminates the need for intermediaries, streamlining operations and reducing costs. Smart contracts, self-executing agreements stored on the blockchain, automate complex processes, minimizing the risk of errors and fraud. This automation fosters greater efficiency and transparency, building trust among participants.

The impact of blockchain on payments is particularly profound. Cryptocurrencies, powered by blockchain, offer a fast and cost-effective alternative to traditional payment methods. Cross-border transactions, which traditionally took days to complete, can now be settled in real-time. This efficiency benefits both businesses and individuals, facilitating global trade and financial inclusion.

Beyond traditional payments, blockchain is enabling new financial services like decentralized finance (DeFi). DeFi platforms offer a wide range of financial products, including lending, borrowing, and trading, directly to users without the need for traditional financial institutions. This opens up opportunities for financial innovation and empowers individuals with greater control over their finances.

As blockchain technology continues to evolve, its impact on financial services will only intensify. With its ability to enhance security, speed up transactions, and reduce costs, blockchain is poised to revolutionize how we manage and interact with money in the years to come.

Healthcare: Securing Medical Records and Data Exchange

Blockchain technology is revolutionizing industries, and healthcare is no exception. The decentralized, secure, and transparent nature of blockchain offers a powerful solution to the challenges of securing medical records and facilitating efficient data exchange.

Traditionally, healthcare records have been stored in centralized databases, vulnerable to breaches and unauthorized access. Blockchain’s distributed ledger technology creates a tamper-proof and immutable record of all medical data, enhancing security and privacy.

With blockchain, patients can have complete control over their medical data, granting access only to authorized parties. This empowers patients to manage their health information, share it with healthcare providers, and even monetize it if they choose.

Blockchain can streamline data exchange between healthcare providers, reducing administrative burdens and improving efficiency. For example, a patient’s medical history can be securely shared between hospitals, ensuring accurate and up-to-date information during treatment.

The secure and transparent nature of blockchain can also foster trust and collaboration in healthcare. This is particularly relevant for clinical trials, where data integrity and transparency are paramount.

While the adoption of blockchain in healthcare is still in its early stages, its potential to transform the industry is immense. By ensuring secure data management, facilitating seamless data exchange, and promoting patient empowerment, blockchain is poised to revolutionize the healthcare landscape.

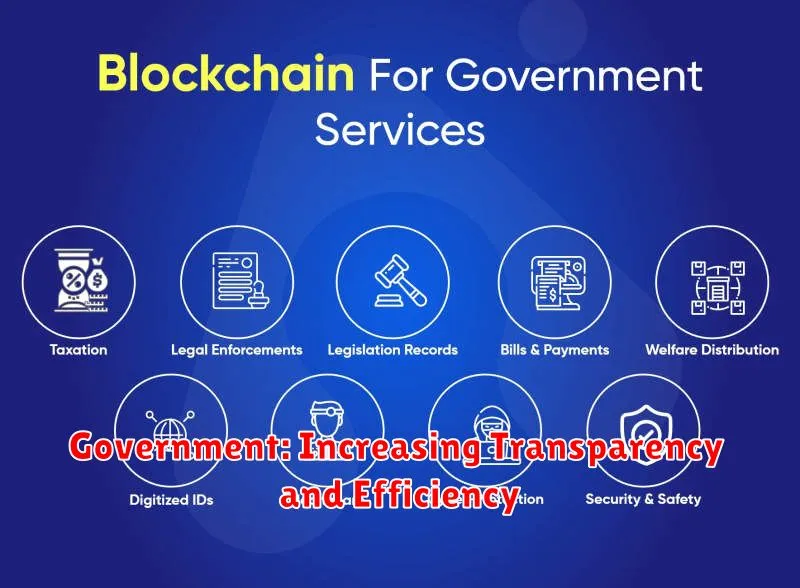

Government: Increasing Transparency and Efficiency

Blockchain technology is not only revolutionizing the business world but also transforming the way governments operate. By offering a secure, transparent, and efficient platform for record-keeping and data management, blockchain can significantly enhance government operations and public trust. The immutable and decentralized nature of blockchain makes it virtually tamper-proof, eliminating the possibility of fraudulent activities and ensuring the integrity of official records. This transparency fosters accountability, as every transaction and data entry is recorded on the blockchain, making it easily auditable and accessible to the public.

Moreover, blockchain can streamline government processes, making them more efficient and cost-effective. For instance, land registry systems can be digitized and automated, reducing bureaucratic delays and improving the speed of property transactions. Similarly, supply chain management for public goods can be optimized, ensuring transparency and reducing the risk of corruption. This increased efficiency translates into savings for the government and a better overall experience for citizens.

Furthermore, blockchain can be leveraged to facilitate secure and efficient electronic voting systems. By using a blockchain-based platform, votes can be cast securely and anonymously, eliminating the possibility of fraud or manipulation. This fosters greater trust in the electoral process and empowers citizens to participate more actively in democratic governance.

The implementation of blockchain technology in government services promises a future where government operations are more transparent, efficient, and trustworthy. By embracing this transformative technology, governments can build a more accountable and responsive public sector that better serves the needs of its citizens.

Real Estate: Streamlining Property Transactions

Blockchain technology is transforming industries, including the real estate sector, by streamlining property transactions. Smart contracts, enabled by blockchain, automate and expedite various stages of the real estate process, such as escrow, title transfer, and property registration.

With blockchain, property records are stored securely and transparently on a distributed ledger. This eliminates the need for intermediaries, reducing transaction costs, and increasing efficiency. Real-time property information is accessible to all authorized parties, fostering greater transparency and accountability.

Digital property ownership records stored on the blockchain are tamper-proof, reducing the risk of fraud and disputes. This enhances trust and confidence in property transactions, while also facilitating faster and smoother closings.

The potential of blockchain in real estate is vast, promising a more transparent, secure, and efficient property market. By embracing this technology, the real estate industry can unlock significant benefits for both buyers and sellers.

Benefits of Implementing Blockchain for Businesses

Blockchain technology is revolutionizing the way businesses operate across various industries. It offers numerous benefits that can significantly enhance efficiency, security, and transparency. Implementing blockchain can empower businesses to transform their operations, streamline processes, and gain a competitive edge.

One of the most significant benefits of blockchain is its enhanced security. Blockchain uses cryptography and decentralized ledgers to create a tamper-proof record of transactions. This eliminates the risk of data breaches and fraud, ensuring the integrity of data and transactions. Businesses can rely on blockchain to protect sensitive information and build trust with stakeholders.

Blockchain also promotes transparency and accountability. All transactions are recorded on the blockchain, making them publicly auditable. This transparency fosters trust among participants and reduces the likelihood of disputes. Businesses can leverage blockchain to improve their supply chain management, track goods, and ensure ethical sourcing.

Furthermore, blockchain enables efficient and cost-effective operations. By eliminating intermediaries and automating processes, blockchain reduces administrative overhead and streamlines transactions. Businesses can achieve faster settlement times, reduce paperwork, and optimize resource allocation.

Blockchain technology also facilitates smart contracts, which are self-executing agreements that automatically enforce the terms of a contract. This eliminates the need for manual intervention, reducing the risk of errors and disputes. Smart contracts empower businesses to automate processes, improve efficiency, and reduce legal and administrative costs.

In conclusion, implementing blockchain offers numerous benefits for businesses, including enhanced security, transparency, efficiency, and cost-effectiveness. By embracing blockchain technology, businesses can transform their operations, gain a competitive advantage, and unlock new opportunities for growth and innovation.

Enhanced Security and Reduced Fraud

Blockchain technology is revolutionizing the business landscape by offering a secure and transparent platform for transactions. One of its most significant advantages is the enhanced security and reduced fraud it provides. Unlike traditional systems that rely on centralized databases, blockchain utilizes a decentralized network, making it highly resistant to manipulation or hacking.

Each transaction on a blockchain is recorded on a distributed ledger, shared across multiple computers in the network. This creates an immutable record of transactions, making it virtually impossible to alter or delete data. The cryptographic nature of blockchain further strengthens security by encrypting data, making it inaccessible to unauthorized individuals.

The decentralized nature of blockchain also eliminates the need for a central authority to manage and validate transactions, reducing the risk of fraud. By removing intermediaries, blockchain enables direct peer-to-peer transactions, increasing transparency and trust. This significantly reduces the potential for manipulation or fraudulent activities.

Furthermore, blockchain technology facilitates the creation of smart contracts, self-executing agreements that automate processes and eliminate the need for manual intervention. Smart contracts ensure that transactions are executed only when predetermined conditions are met, further reducing the risk of fraud and human error.

The combination of these features makes blockchain a powerful tool for enhancing security and reducing fraud in various industries. From supply chain management to financial transactions, blockchain’s inherent transparency, immutability, and security make it an ideal solution for streamlining operations and mitigating risks.

Increased Transparency and Trust

Blockchain technology has emerged as a transformative force across various industries, revolutionizing the way businesses operate and interact. One of the most significant benefits of blockchain is its ability to enhance transparency and trust, creating a more reliable and accountable ecosystem.

At its core, blockchain is a distributed ledger that records transactions across a network of computers. This decentralized nature ensures that data is immutable and tamper-proof, creating an auditable trail that can be accessed by all participants. This immutability eliminates the need for intermediaries and fosters trust among parties, as any attempt to alter the record would be immediately visible to everyone on the network.

The transparent nature of blockchain empowers businesses to build trust and accountability within their operations and with their stakeholders. By providing a verifiable and auditable history of transactions, blockchain eliminates the potential for fraud, manipulation, and data breaches. This enhanced transparency fosters greater trust in supply chains, financial transactions, and other critical business processes.

Furthermore, blockchain’s ability to track the provenance of goods and services strengthens transparency and traceability. By recording the origin, movement, and ownership of products throughout the supply chain, blockchain allows businesses to ensure the authenticity and quality of their offerings. This is particularly valuable in industries such as agriculture, pharmaceuticals, and luxury goods, where counterfeit products pose a significant threat.

In conclusion, blockchain technology offers a powerful solution for increasing transparency and trust within business operations. By establishing a tamper-proof record of transactions and empowering stakeholders with access to verifiable data, blockchain fosters greater accountability, reduces fraud, and strengthens relationships. As blockchain continues to evolve, its impact on transparency and trust will undoubtedly shape the future of business.

Improved Efficiency and Reduced Costs

One of the most significant benefits of blockchain technology is its ability to streamline processes and reduce operational costs. By eliminating intermediaries and automating tasks, businesses can achieve greater efficiency and significant cost savings.

For example, in supply chain management, blockchain can track products from origin to destination, reducing the risk of counterfeiting and fraud. This transparency and traceability allow for faster and more efficient inventory management, leading to reduced costs and improved delivery times.

Furthermore, blockchain’s decentralized nature eliminates the need for central authorities, such as banks or clearing houses, to handle transactions. This reduces transaction fees and processing time, making it more cost-effective for businesses.

The immutability and security of blockchain technology also contribute to reduced costs. With tamper-proof records, businesses can minimize disputes and litigation, saving on legal fees and settlements.

By leveraging blockchain’s potential for automation, transparency, and security, businesses can significantly improve their efficiency and reduce operational costs, leading to increased profitability and a competitive edge.

Challenges and Considerations for Blockchain Adoption

While blockchain technology holds immense potential for transforming industries and revolutionizing operations, its adoption faces various challenges and considerations. These factors play a crucial role in determining the successful integration of blockchain into existing business processes and systems.

Scalability remains a major obstacle. Existing blockchain platforms struggle to handle large volumes of transactions, limiting their applicability to real-world scenarios demanding high throughput.

Interoperability poses another challenge. The fragmented landscape of blockchain platforms hampers seamless communication and data exchange between different networks. This lack of interoperability hinders the potential for collaborative solutions and hinders wider adoption.

Regulation presents significant challenges. The decentralized nature of blockchain technology poses difficulties for regulatory authorities in terms of oversight and compliance.

Security concerns linger as well. While blockchain offers enhanced security through its decentralized and immutable nature, vulnerabilities exist, such as smart contract bugs and potential attacks. Robust security measures are essential for building trust and confidence in the technology.

Cost can be a deterrent for widespread adoption. The infrastructure required for blockchain implementation, including hardware, software, and expertise, can be substantial, especially for smaller businesses.

Talent is another critical consideration. Organizations need skilled professionals with expertise in blockchain technology to develop, implement, and manage solutions. The scarcity of qualified individuals presents a hurdle for many companies.

Despite these challenges, the transformative potential of blockchain technology remains compelling. By carefully addressing these considerations, businesses can unlock the benefits of this revolutionary technology and shape the future of industries worldwide.

Overcoming Regulatory and Legal Hurdles

While blockchain technology promises transformative benefits for businesses, it faces significant regulatory and legal hurdles. Transparency and security concerns are at the forefront, as regulators grapple with understanding and overseeing this new technology. Data privacy regulations like GDPR are also a key consideration, especially with the potential for sensitive data to be stored and shared on blockchain networks.

Legal frameworks are still evolving to address the unique characteristics of blockchain. Smart contracts, for instance, raise questions about enforceability and liability, while the decentralized nature of blockchain raises concerns about jurisdiction and regulatory oversight. Tokenization, the process of converting assets into digital tokens, also faces challenges with existing securities laws.

Overcoming these hurdles requires collaboration between businesses, regulators, and industry experts. Clear regulations are essential to foster innovation and provide legal certainty. Education and awareness are crucial to address concerns and build trust in blockchain technology. Ultimately, a robust regulatory framework that balances innovation and consumer protection is critical for the widespread adoption of blockchain in business.

Addressing Scalability and Interoperability Issues

While blockchain technology holds immense potential for transforming industries, it faces two primary challenges: scalability and interoperability.

Scalability refers to the ability of a blockchain network to handle a large volume of transactions efficiently. Many blockchains, including Bitcoin, have limited transaction throughput, leading to congestion and high transaction fees during peak periods. This hinders their adoption for large-scale business applications.

Interoperability, on the other hand, focuses on the seamless communication and data exchange between different blockchain networks. Currently, blockchains operate in silos, hindering their ability to work together and create a truly interconnected ecosystem. This lack of interoperability limits the potential for cross-chain collaboration and data sharing.

To address these issues, researchers and developers are exploring various solutions. Sharding, a technique that divides the blockchain into smaller, more manageable fragments, is one approach to enhance scalability. Another solution is the development of layer-2 scaling solutions, which build on existing blockchains to improve transaction speeds and reduce costs.

Interoperability is being addressed through the development of cross-chain protocols and interoperability platforms. These initiatives aim to create bridges between different blockchains, enabling data transfer and communication between them.

Overcoming scalability and interoperability challenges is crucial for the wider adoption of blockchain technology in business. As these issues are addressed, we can expect to see more innovative and transformative applications of blockchain across industries.

The Future of Blockchain in the Business Landscape

Blockchain technology has emerged as a transformative force across industries, revolutionizing the way businesses operate and interact. As we look towards the future, blockchain’s impact is poised to become even more profound, shaping the business landscape in unprecedented ways. From enhancing security and transparency to streamlining processes and fostering innovation, the potential of blockchain is vast.

One of the most significant future trends is the increasing adoption of blockchain across various sectors. Supply chain management is poised for a major transformation, as blockchain enables real-time tracking of goods, reducing fraud and improving efficiency. In finance, decentralized finance (DeFi) platforms are gaining traction, offering innovative financial services like lending and borrowing without intermediaries. The healthcare industry can leverage blockchain to securely store and share patient data, while the public sector can use it to enhance voting systems and ensure transparency.

Beyond individual industries, blockchain is set to foster a more interconnected and collaborative business environment. Interoperability, the ability of different blockchain networks to communicate with each other, will become increasingly important, enabling seamless data sharing and cross-industry collaborations. As blockchain matures, we can expect to see the emergence of decentralized autonomous organizations (DAOs), which are self-governing entities based on blockchain principles, potentially changing the way companies are structured and managed.

While the future of blockchain in the business landscape is bright, there are still challenges to overcome. Scalability, regulatory uncertainty, and security concerns need to be addressed to ensure widespread adoption. However, with continued research and development, these obstacles are gradually being overcome, paving the way for a future where blockchain plays a central role in shaping the business world.

{kind=link}